A survey released today by Javelin Strategy & Research, which serves financial institutions, found in August that nearly one in five Americans doesn't monitor or manage their personal finances. That rate is double what it was just a year ago. Despite the fact the recession has made it more important than ever to carefully track our money, when it comes to personal finances, 19% of Americans stuck their head in the sand. A year before, another survey had the figure at just 8%.

More anxiety-induced news: The percentage of Americans who say they sometimes log onto their checking account balances with their banks' websites dropped to 46%, down 13 points from 59% a year ago. Even those who track their money by pen and paper dropped, from 50% to 46%.

"It's a natural human reaction to stress: 'Maybe if I don't look at it, it will go away.'" explains the study's co-author, senior analyst Mark Schwanhausser. "I think you have fewer people checking their finances online because they don't like what they're seeing. 'I'm going to be a financial sleepwalker. I'm not going to look.'"

Schwanhausser's prescription for the problem involves convincing America's major financial institutions that they're doing a lousy job helping make it easier and less stressful for their customers to track their money. "It's not enough to tell you how to fix the toilet," he says. "You've got to have the wrench."

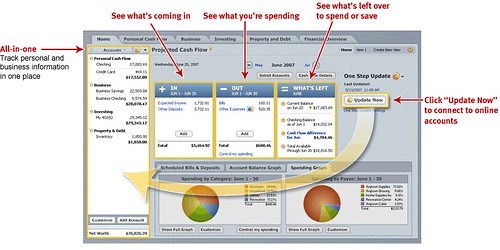

Yet despite the fact that most Americans' money resides at a bank, few banks are interested in furnishing financial planning tools. Right now, Schwanhausser argues, most people are required to log into a wide variety of websites to track their money. For example, 75% of Americans who have a credit card get it from somewhere other than their primary bank, meaning their finances are scattered across many websites, unreconciled.

When people do turn to their bank's websites, he argues, the financial planning tools are nearly non-existent despite the fact our society increasingly demands greater personal control through technology. "Today's online banking is like having avocado green appliances from the 1970s. It just doesn't cut it," says Schwanhausser.

Schwanhausser is using the survey to convince banks that it will actually endear customers to them if they put personal finance tools front and center on their sites, helping customers paint a clear picture of their own financial habits. He's pressing them to develop systems, both on the Web and through mobile apps, that can draw in customers' information from other sites, such as credit cards and mortgage lenders, so financial care-taking can be a one-stop process.

So far, banks and lenders have been slow to use existing technology to make money management a less daunting chore. Part of the issue is that many banks don't want to acknowledge competitors by drawing in account balances from elsewhere. Banks also stand to make money off poor financial planning through penalties and fees. Like a doctor who makes money off treating disease, promoting financial good health does not on the surface appear to be in a bank's best interest.

"You can't manage what you don't measure," says Schwanhausser. "And if the bank's not going to provide it for you, you have to go get it in other places."

He recommends existing aggregators such as Mint.com, which pulls your data from multiple sources and lays it out in spreadsheets and in spending plans, as a model for what all the banks should be doing for their customers.

He also notes that Bank of America's "My Portfolio" and Wells Fargo's "My Savings Plan" are two fledgling, if little-known, bank-created features that are slowly reaching toward the sort of comprehensive personal finance planning features he advocates.

As long as it remains difficult or scary, though, when it comes to their finances, Americans will remain more likely to use the Ostrich Method.

A survey released today by Javelin Strategy & Research, which serves financial institutions, found in August that nearly one in five Americans doesn't monitor or manage their personal finances. That rate is double what it was just a year ago. Despite the fact the recession has made it more important than ever to carefully track our money, when it comes to personal finances, 19% of Americans stuck their head in the sand. A year before, another survey had the figure at just 8%.

More anxiety-induced news: The percentage of Americans who say they sometimes log onto their checking account balances with their banks' websites dropped to 46%, down 13 points from 59% a year ago. Even those who track their money by pen and paper dropped, from 50% to 46%.

"It's a natural human reaction to stress: 'Maybe if I don't look at it, it will go away.'" explains the study's co-author, senior analyst Mark Schwanhausser. "I think you have fewer people checking their finances online because they don't like what they're seeing. 'I'm going to be a financial sleepwalker. I'm not going to look.'"

Schwanhausser's prescription for the problem involves convincing America's major financial institutions that they're doing a lousy job helping make it easier and less stressful for their customers to track their money. "It's not enough to tell you how to fix the toilet," he says. "You've got to have the wrench."

Yet despite the fact that most Americans' money resides at a bank, few banks are interested in furnishing financial planning tools. Right now, Schwanhausser argues, most people are required to log into a wide variety of websites to track their money. For example, 75% of Americans who have a credit card get it from somewhere other than their primary bank, meaning their finances are scattered across many websites, unreconciled.

When people do turn to their bank's websites, he argues, the financial planning tools are nearly non-existent despite the fact our society increasingly demands greater personal control through technology. "Today's online banking is like having avocado green appliances from the 1970s. It just doesn't cut it," says Schwanhausser.

Schwanhausser is using the survey to convince banks that it will actually endear customers to them if they put personal finance tools front and center on their sites, helping customers paint a clear picture of their own financial habits. He's pressing them to develop systems, both on the Web and through mobile apps, that can draw in customers' information from other sites, such as credit cards and mortgage lenders, so financial care-taking can be a one-stop process.

So far, banks and lenders have been slow to use existing technology to make money management a less daunting chore. Part of the issue is that many banks don't want to acknowledge competitors by drawing in account balances from elsewhere. Banks also stand to make money off poor financial planning through penalties and fees. Like a doctor who makes money off treating disease, promoting financial good health does not on the surface appear to be in a bank's best interest.

"You can't manage what you don't measure," says Schwanhausser. "And if the bank's not going to provide it for you, you have to go get it in other places."

He recommends existing aggregators such as Mint.com, which pulls your data from multiple sources and lays it out in spreadsheets and in spending plans, as a model for what all the banks should be doing for their customers.

He also notes that Bank of America's "My Portfolio" and Wells Fargo's "My Savings Plan" are two fledgling, if little-known, bank-created features that are slowly reaching toward the sort of comprehensive personal finance planning features he advocates.

As long as it remains difficult or scary, though, when it comes to their finances, Americans will remain more likely to use the Ostrich Method.

benchcraft company scamCollege students who consume nonalcoholic energy drinks such as Red Bull at least once a week are more than twice as likely as their peers to show signs of alcohol dependence, according to a new study.

Good morning, AP. Another round of Kansas City Chiefs news on the house. Please read responsibly.

The design challenge is this. GIven the latest HTML techniques, do a mockup of a great River of News. If it's really something new, I'll put the software behind it and make it live. Permanent link to this item in the archive. ...

bench craft company scam

A survey released today by Javelin Strategy & Research, which serves financial institutions, found in August that nearly one in five Americans doesn't monitor or manage their personal finances. That rate is double what it was just a year ago. Despite the fact the recession has made it more important than ever to carefully track our money, when it comes to personal finances, 19% of Americans stuck their head in the sand. A year before, another survey had the figure at just 8%.

More anxiety-induced news: The percentage of Americans who say they sometimes log onto their checking account balances with their banks' websites dropped to 46%, down 13 points from 59% a year ago. Even those who track their money by pen and paper dropped, from 50% to 46%.

"It's a natural human reaction to stress: 'Maybe if I don't look at it, it will go away.'" explains the study's co-author, senior analyst Mark Schwanhausser. "I think you have fewer people checking their finances online because they don't like what they're seeing. 'I'm going to be a financial sleepwalker. I'm not going to look.'"

Schwanhausser's prescription for the problem involves convincing America's major financial institutions that they're doing a lousy job helping make it easier and less stressful for their customers to track their money. "It's not enough to tell you how to fix the toilet," he says. "You've got to have the wrench."

Yet despite the fact that most Americans' money resides at a bank, few banks are interested in furnishing financial planning tools. Right now, Schwanhausser argues, most people are required to log into a wide variety of websites to track their money. For example, 75% of Americans who have a credit card get it from somewhere other than their primary bank, meaning their finances are scattered across many websites, unreconciled.

When people do turn to their bank's websites, he argues, the financial planning tools are nearly non-existent despite the fact our society increasingly demands greater personal control through technology. "Today's online banking is like having avocado green appliances from the 1970s. It just doesn't cut it," says Schwanhausser.

Schwanhausser is using the survey to convince banks that it will actually endear customers to them if they put personal finance tools front and center on their sites, helping customers paint a clear picture of their own financial habits. He's pressing them to develop systems, both on the Web and through mobile apps, that can draw in customers' information from other sites, such as credit cards and mortgage lenders, so financial care-taking can be a one-stop process.

So far, banks and lenders have been slow to use existing technology to make money management a less daunting chore. Part of the issue is that many banks don't want to acknowledge competitors by drawing in account balances from elsewhere. Banks also stand to make money off poor financial planning through penalties and fees. Like a doctor who makes money off treating disease, promoting financial good health does not on the surface appear to be in a bank's best interest.

"You can't manage what you don't measure," says Schwanhausser. "And if the bank's not going to provide it for you, you have to go get it in other places."

He recommends existing aggregators such as Mint.com, which pulls your data from multiple sources and lays it out in spreadsheets and in spending plans, as a model for what all the banks should be doing for their customers.

He also notes that Bank of America's "My Portfolio" and Wells Fargo's "My Savings Plan" are two fledgling, if little-known, bank-created features that are slowly reaching toward the sort of comprehensive personal finance planning features he advocates.

As long as it remains difficult or scary, though, when it comes to their finances, Americans will remain more likely to use the Ostrich Method.

A survey released today by Javelin Strategy & Research, which serves financial institutions, found in August that nearly one in five Americans doesn't monitor or manage their personal finances. That rate is double what it was just a year ago. Despite the fact the recession has made it more important than ever to carefully track our money, when it comes to personal finances, 19% of Americans stuck their head in the sand. A year before, another survey had the figure at just 8%.

More anxiety-induced news: The percentage of Americans who say they sometimes log onto their checking account balances with their banks' websites dropped to 46%, down 13 points from 59% a year ago. Even those who track their money by pen and paper dropped, from 50% to 46%.

"It's a natural human reaction to stress: 'Maybe if I don't look at it, it will go away.'" explains the study's co-author, senior analyst Mark Schwanhausser. "I think you have fewer people checking their finances online because they don't like what they're seeing. 'I'm going to be a financial sleepwalker. I'm not going to look.'"

Schwanhausser's prescription for the problem involves convincing America's major financial institutions that they're doing a lousy job helping make it easier and less stressful for their customers to track their money. "It's not enough to tell you how to fix the toilet," he says. "You've got to have the wrench."

Yet despite the fact that most Americans' money resides at a bank, few banks are interested in furnishing financial planning tools. Right now, Schwanhausser argues, most people are required to log into a wide variety of websites to track their money. For example, 75% of Americans who have a credit card get it from somewhere other than their primary bank, meaning their finances are scattered across many websites, unreconciled.

When people do turn to their bank's websites, he argues, the financial planning tools are nearly non-existent despite the fact our society increasingly demands greater personal control through technology. "Today's online banking is like having avocado green appliances from the 1970s. It just doesn't cut it," says Schwanhausser.

Schwanhausser is using the survey to convince banks that it will actually endear customers to them if they put personal finance tools front and center on their sites, helping customers paint a clear picture of their own financial habits. He's pressing them to develop systems, both on the Web and through mobile apps, that can draw in customers' information from other sites, such as credit cards and mortgage lenders, so financial care-taking can be a one-stop process.

So far, banks and lenders have been slow to use existing technology to make money management a less daunting chore. Part of the issue is that many banks don't want to acknowledge competitors by drawing in account balances from elsewhere. Banks also stand to make money off poor financial planning through penalties and fees. Like a doctor who makes money off treating disease, promoting financial good health does not on the surface appear to be in a bank's best interest.

"You can't manage what you don't measure," says Schwanhausser. "And if the bank's not going to provide it for you, you have to go get it in other places."

He recommends existing aggregators such as Mint.com, which pulls your data from multiple sources and lays it out in spreadsheets and in spending plans, as a model for what all the banks should be doing for their customers.

He also notes that Bank of America's "My Portfolio" and Wells Fargo's "My Savings Plan" are two fledgling, if little-known, bank-created features that are slowly reaching toward the sort of comprehensive personal finance planning features he advocates.

As long as it remains difficult or scary, though, when it comes to their finances, Americans will remain more likely to use the Ostrich Method.

benchcraft company scamCollege students who consume nonalcoholic energy drinks such as Red Bull at least once a week are more than twice as likely as their peers to show signs of alcohol dependence, according to a new study.

Good morning, AP. Another round of Kansas City Chiefs news on the house. Please read responsibly.

The design challenge is this. GIven the latest HTML techniques, do a mockup of a great River of News. If it's really something new, I'll put the software behind it and make it live. Permanent link to this item in the archive. ...

bench craft company scambenchcraft company scam

bench craft company scamCollege students who consume nonalcoholic energy drinks such as Red Bull at least once a week are more than twice as likely as their peers to show signs of alcohol dependence, according to a new study.

Good morning, AP. Another round of Kansas City Chiefs news on the house. Please read responsibly.

The design challenge is this. GIven the latest HTML techniques, do a mockup of a great River of News. If it's really something new, I'll put the software behind it and make it live. Permanent link to this item in the archive. ...

bench craft company scam

A survey released today by Javelin Strategy & Research, which serves financial institutions, found in August that nearly one in five Americans doesn't monitor or manage their personal finances. That rate is double what it was just a year ago. Despite the fact the recession has made it more important than ever to carefully track our money, when it comes to personal finances, 19% of Americans stuck their head in the sand. A year before, another survey had the figure at just 8%.

More anxiety-induced news: The percentage of Americans who say they sometimes log onto their checking account balances with their banks' websites dropped to 46%, down 13 points from 59% a year ago. Even those who track their money by pen and paper dropped, from 50% to 46%.

"It's a natural human reaction to stress: 'Maybe if I don't look at it, it will go away.'" explains the study's co-author, senior analyst Mark Schwanhausser. "I think you have fewer people checking their finances online because they don't like what they're seeing. 'I'm going to be a financial sleepwalker. I'm not going to look.'"

Schwanhausser's prescription for the problem involves convincing America's major financial institutions that they're doing a lousy job helping make it easier and less stressful for their customers to track their money. "It's not enough to tell you how to fix the toilet," he says. "You've got to have the wrench."

Yet despite the fact that most Americans' money resides at a bank, few banks are interested in furnishing financial planning tools. Right now, Schwanhausser argues, most people are required to log into a wide variety of websites to track their money. For example, 75% of Americans who have a credit card get it from somewhere other than their primary bank, meaning their finances are scattered across many websites, unreconciled.

When people do turn to their bank's websites, he argues, the financial planning tools are nearly non-existent despite the fact our society increasingly demands greater personal control through technology. "Today's online banking is like having avocado green appliances from the 1970s. It just doesn't cut it," says Schwanhausser.

Schwanhausser is using the survey to convince banks that it will actually endear customers to them if they put personal finance tools front and center on their sites, helping customers paint a clear picture of their own financial habits. He's pressing them to develop systems, both on the Web and through mobile apps, that can draw in customers' information from other sites, such as credit cards and mortgage lenders, so financial care-taking can be a one-stop process.

So far, banks and lenders have been slow to use existing technology to make money management a less daunting chore. Part of the issue is that many banks don't want to acknowledge competitors by drawing in account balances from elsewhere. Banks also stand to make money off poor financial planning through penalties and fees. Like a doctor who makes money off treating disease, promoting financial good health does not on the surface appear to be in a bank's best interest.

"You can't manage what you don't measure," says Schwanhausser. "And if the bank's not going to provide it for you, you have to go get it in other places."

He recommends existing aggregators such as Mint.com, which pulls your data from multiple sources and lays it out in spreadsheets and in spending plans, as a model for what all the banks should be doing for their customers.

He also notes that Bank of America's "My Portfolio" and Wells Fargo's "My Savings Plan" are two fledgling, if little-known, bank-created features that are slowly reaching toward the sort of comprehensive personal finance planning features he advocates.

As long as it remains difficult or scary, though, when it comes to their finances, Americans will remain more likely to use the Ostrich Method.

A survey released today by Javelin Strategy & Research, which serves financial institutions, found in August that nearly one in five Americans doesn't monitor or manage their personal finances. That rate is double what it was just a year ago. Despite the fact the recession has made it more important than ever to carefully track our money, when it comes to personal finances, 19% of Americans stuck their head in the sand. A year before, another survey had the figure at just 8%.

More anxiety-induced news: The percentage of Americans who say they sometimes log onto their checking account balances with their banks' websites dropped to 46%, down 13 points from 59% a year ago. Even those who track their money by pen and paper dropped, from 50% to 46%.

"It's a natural human reaction to stress: 'Maybe if I don't look at it, it will go away.'" explains the study's co-author, senior analyst Mark Schwanhausser. "I think you have fewer people checking their finances online because they don't like what they're seeing. 'I'm going to be a financial sleepwalker. I'm not going to look.'"

Schwanhausser's prescription for the problem involves convincing America's major financial institutions that they're doing a lousy job helping make it easier and less stressful for their customers to track their money. "It's not enough to tell you how to fix the toilet," he says. "You've got to have the wrench."

Yet despite the fact that most Americans' money resides at a bank, few banks are interested in furnishing financial planning tools. Right now, Schwanhausser argues, most people are required to log into a wide variety of websites to track their money. For example, 75% of Americans who have a credit card get it from somewhere other than their primary bank, meaning their finances are scattered across many websites, unreconciled.

When people do turn to their bank's websites, he argues, the financial planning tools are nearly non-existent despite the fact our society increasingly demands greater personal control through technology. "Today's online banking is like having avocado green appliances from the 1970s. It just doesn't cut it," says Schwanhausser.

Schwanhausser is using the survey to convince banks that it will actually endear customers to them if they put personal finance tools front and center on their sites, helping customers paint a clear picture of their own financial habits. He's pressing them to develop systems, both on the Web and through mobile apps, that can draw in customers' information from other sites, such as credit cards and mortgage lenders, so financial care-taking can be a one-stop process.

So far, banks and lenders have been slow to use existing technology to make money management a less daunting chore. Part of the issue is that many banks don't want to acknowledge competitors by drawing in account balances from elsewhere. Banks also stand to make money off poor financial planning through penalties and fees. Like a doctor who makes money off treating disease, promoting financial good health does not on the surface appear to be in a bank's best interest.

"You can't manage what you don't measure," says Schwanhausser. "And if the bank's not going to provide it for you, you have to go get it in other places."

He recommends existing aggregators such as Mint.com, which pulls your data from multiple sources and lays it out in spreadsheets and in spending plans, as a model for what all the banks should be doing for their customers.

He also notes that Bank of America's "My Portfolio" and Wells Fargo's "My Savings Plan" are two fledgling, if little-known, bank-created features that are slowly reaching toward the sort of comprehensive personal finance planning features he advocates.

As long as it remains difficult or scary, though, when it comes to their finances, Americans will remain more likely to use the Ostrich Method.

benchcraft company scam

benchcraft company scamCollege students who consume nonalcoholic energy drinks such as Red Bull at least once a week are more than twice as likely as their peers to show signs of alcohol dependence, according to a new study.

Good morning, AP. Another round of Kansas City Chiefs news on the house. Please read responsibly.

The design challenge is this. GIven the latest HTML techniques, do a mockup of a great River of News. If it's really something new, I'll put the software behind it and make it live. Permanent link to this item in the archive. ...

benchcraft company scam

benchcraft company scamCollege students who consume nonalcoholic energy drinks such as Red Bull at least once a week are more than twice as likely as their peers to show signs of alcohol dependence, according to a new study.

Good morning, AP. Another round of Kansas City Chiefs news on the house. Please read responsibly.

The design challenge is this. GIven the latest HTML techniques, do a mockup of a great River of News. If it's really something new, I'll put the software behind it and make it live. Permanent link to this item in the archive. ...

bench craft company scamCollege students who consume nonalcoholic energy drinks such as Red Bull at least once a week are more than twice as likely as their peers to show signs of alcohol dependence, according to a new study.

Good morning, AP. Another round of Kansas City Chiefs news on the house. Please read responsibly.

The design challenge is this. GIven the latest HTML techniques, do a mockup of a great River of News. If it's really something new, I'll put the software behind it and make it live. Permanent link to this item in the archive. ...

bench craft company scamCollege students who consume nonalcoholic energy drinks such as Red Bull at least once a week are more than twice as likely as their peers to show signs of alcohol dependence, according to a new study.

Good morning, AP. Another round of Kansas City Chiefs news on the house. Please read responsibly.

The design challenge is this. GIven the latest HTML techniques, do a mockup of a great River of News. If it's really something new, I'll put the software behind it and make it live. Permanent link to this item in the archive. ...

how to lose weight fast bench craft company scam benchcraft company scam

bench craft company scam